Table of Contents

ToggleIntroduction

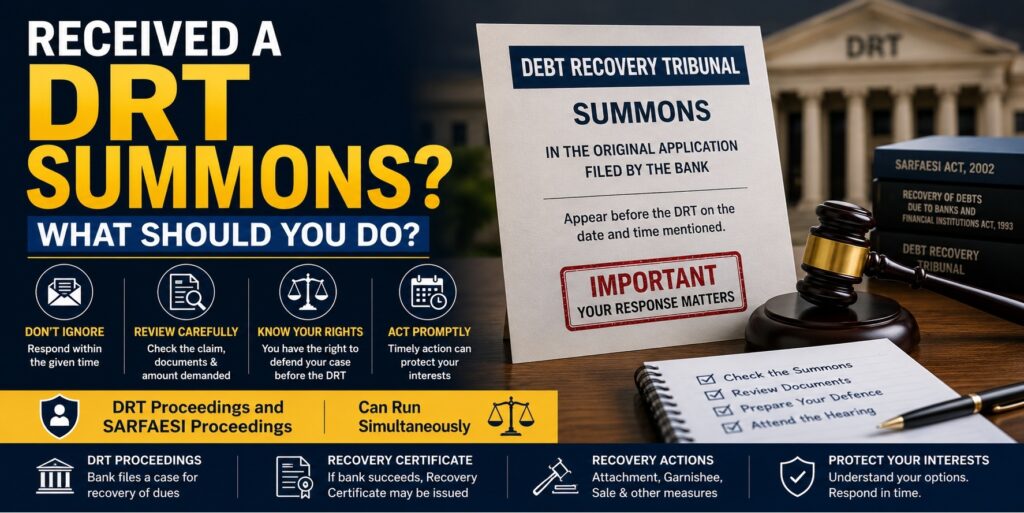

Receiving a summons from the Debt Recovery Tribunal (DRT) can be alarming. Many borrowers assume that once a DRT summons is received, the bank has already won the case or that immediate attachment of property will follow.

In reality, a DRT summons is simply the formal commencement of legal proceedings by a bank or financial institution seeking recovery of its dues.

Understanding what the summons means—and what it does not mean—is important for protecting your legal rights.

What Is a DRT Summons?

A DRT summons is issued after a bank or financial institution files an Original Application (O.A.) before the Debt Recovery Tribunal seeking recovery of a debt.

The summons generally requires the borrower, guarantor, or other defendants to:

* Appear before the Tribunal.

* File their defence.

* Respond to the allegations made by the bank.

The summons is often accompanied by:

* Copy of the Original Application.

* Statement of claim.

* Loan documents.

* Statement of account.

* Other supporting records.

Why Has the Bank Approached the DRT?

Banks generally approach the DRT when they seek a formal determination of liability and a Recovery Certificate against the borrower and other liable parties.

The bank may proceed against:

* Borrowers.

* Co-borrowers.

* Personal guarantors.

* Corporate guarantors.

* Mortgagors.

The objective of the bank is usually to obtain a Recovery Certificate that can later be executed through the Recovery Officer.

Does Receiving a DRT Summons Mean the Bank Has Already Won?

No.

The issuance of a summons merely means that proceedings have been initiated.

At this stage, the Tribunal has not yet decided:

* Whether the debt is legally recoverable.

* Whether the amount claimed is correct.

* Whether the borrower or guarantor has valid defences.

* Whether limitation or other legal issues arise.

The summons is intended to provide the defendant an opportunity to contest the claim.

Who Receives DRT Summons?

Depending upon the loan transaction, summons may be issued to:

Borrowers

The principal borrower who availed the credit facility.

Guarantors

Personal guarantors are frequently made parties to DRT proceedings.

Corporate Guarantors

Companies that have furnished guarantees may also be proceeded against.

Mortgagors

Persons who have offered property as security may be impleaded.

Partners of Firms

In partnership-related borrowings, partners may also be made parties.

What Should You Do Immediately After Receiving a DRT Summons?

1.Do Not Ignore the Summons

Ignoring DRT proceedings can result in the matter being heard in your absence.

This may lead to ex parte orders and loss of an opportunity to place your defence before the Tribunal.

2.Read the Original Application Carefully

Examine:

* Amount claimed.

* Date of default.

* Interest calculations.

* Reliefs sought.

* Documents relied upon by the bank.

Many defendants are surprised to discover that the dispute extends beyond the amount they believed was outstanding.

3.Verify the Outstanding Amount

The amount claimed by the bank should be examined carefully.

Common disputes involve:

* Incorrect interest calculations.

* Unaccounted payments.

* Penal charges.

* Errors in the statement of account.

4.Check Whether You Are Sued as Borrower or Guarantor

The legal position of a borrower and guarantor may differ.

Many guarantors wrongly assume that the dispute concerns only the principal borrower.

In reality, guarantors are frequently made jointly and severally liable for the debt.

5.Examine Limitation and Documentation Issues

Depending upon the facts of the case, issues relating to:

* Limitation.

* Revival letters.

* Acknowledgments of debt.

* Guarantee documents.

* Security documents.

may become relevant.

Can SARFAESI Proceedings Continue Even After a DRT Case Is Filed?

Yes.

This is one of the most misunderstood aspects of banking litigation.

Many borrowers assume:

“Once the bank has filed a DRT case, SARFAESI proceedings must stop.”

This is generally incorrect.

In many cases, banks pursue both remedies simultaneously.

For example:

DRT Proceedings:

The bank files an Original Application seeking a Recovery Certificate.

SARFAESI Proceedings:

At the same time, the bank may:

* Issue Section 13(2) notice.

* Take measures under Section 13(4).

* Initiate Section 14 proceedings.

* Take possession of secured assets.

* Conduct auction proceedings.

Accordingly, receiving a DRT summons does not necessarily mean that SARFAESI proceedings have come to an end.

Why Do Banks Use Both DRT and SARFAESI Proceedings?

The answer lies in the difference between the two remedies.

SARFAESI Proceedings

SARFAESI is primarily concerned with enforcement of secured assets.

The bank seeks recovery through the mortgaged property or other secured assets.

DRT Proceedings

The DRT route enables the bank to obtain a Recovery Certificate against the borrower and guarantors.

After a Recovery Certificate is issued, the Recovery Officer may proceed against other assets of the debtor in accordance with law.

For this reason, banks frequently pursue both remedies simultaneously.

What Happens If the Bank Succeeds?

If the Tribunal allows the Original Application, it may issue a Recovery Certificate.

The matter then moves to the Recovery Officer.

Depending upon the circumstances, recovery proceedings may include:

* Attachment of property.

* Attachment of bank accounts.

* Garnishee proceedings.

* Sale of attached assets.

* Other recovery measures permitted by law.

Common Defences Raised in DRT Proceedings

The nature of the defence depends on the facts of each case.

Common issues include:

* Incorrect calculation of dues.

* Limitation.

* Invalid guarantee.

* Settlement-related disputes.

* Defects in documentation.

* Accounting discrepancies.

* Issues relating to security documents.

Common Mistakes Made by Defendants

1.Ignoring the Summons

This is perhaps the most common mistake.

2. Assuming SARFAESI Proceedings Will Automatically Stop

DRT proceedings and SARFAESI proceedings often continue simultaneously.

3.Depending Solely on Oral Assurances

Verbal discussions with bank officials do not automatically suspend legal proceedings.

4.Delaying Preparation of Defence

Important opportunities may be lost by waiting until the last moment.

Conclusion

Receiving a DRT summons should not be ignored, but it should not be viewed as the end of the matter either.

The summons signifies the beginning of a legal process through which the bank seeks recovery of its dues. Borrowers and guarantors continue to possess legal rights and may raise all available factual and legal defences before the Tribunal.

It is equally important to remember that DRT proceedings and SARFAESI proceedings frequently run side by side. Therefore, a person who has received a DRT summons should also verify whether the bank has simultaneously initiated proceedings under the SARFAESI Act.

Understanding the nature of the claim, reviewing the documents carefully, and responding within the prescribed time are often the most important steps after receiving a DRT summons.

Disclaimer: This article is intended for general informational purposes only and does not constitute legal advice. Every case depends upon its own facts, documents and circumstances.