Table of Contents

ToggleIntroduction

In our earlier article titled “Union Budget 2026-27 and the Proposal of Corporate Mitras – Threat or Transformation for Practising CAs, CSs and CMAs?”, we examined the proposal announced by the Hon’ble Finance Minister to create a new cadre of Corporate Mitras and discussed its possible implications for the accounting and compliance professions.

At that stage, the proposal was only a policy announcement. Several important questions remained unanswered. Who would be eligible? What training would be provided? Would Corporate Mitras function independently or under professional supervision? What would be their exact role in the compliance ecosystem?

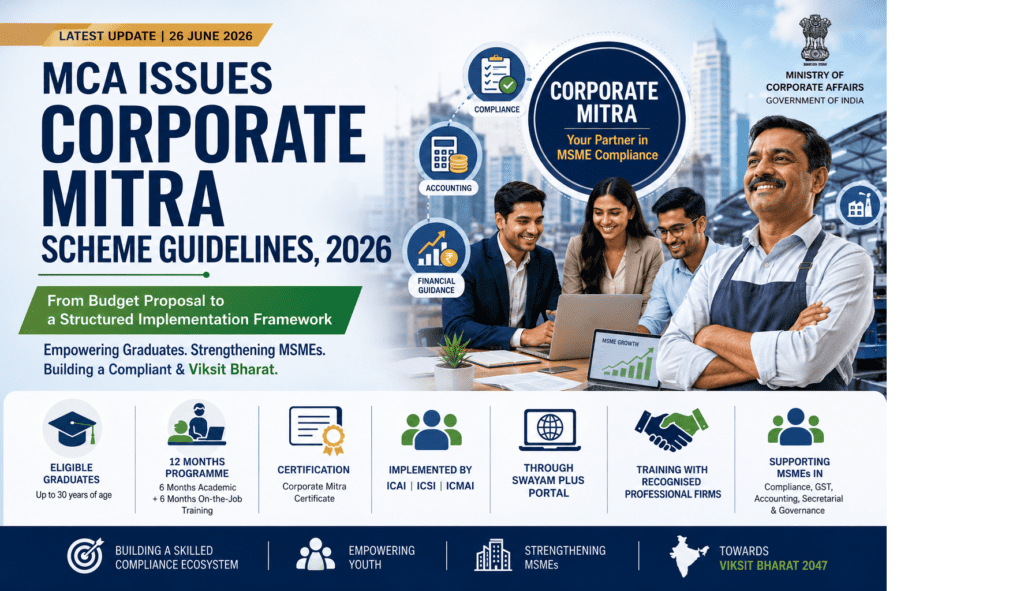

The Ministry of Corporate Affairs (MCA) has now answered many of these questions by issuing the Guidelines for the Corporate Mitra Scheme on 26 June 2026. These Guidelines convert the Budget proposal into a structured implementation framework by prescribing the eligibility criteria, training methodology, certification process, governance structure and implementation mechanism.

This article analyses the salient features of the Guidelines and examines their practical implications for MSMEs, graduates, professional firms and the corporate compliance ecosystem.

From Policy Announcement to Implementation

The Corporate Mitra Scheme was announced in the Union Budget 2026-27 with the objective of strengthening the compliance capabilities of India’s Micro, Small and Medium Enterprises (MSMEs).

The newly issued Guidelines demonstrate that the Government intends to implement the scheme in a structured and professionally supervised manner rather than as a conventional internship or skill-development programme.

Unlike many temporary employment schemes, the Corporate Mitra Scheme has been designed as an independent national initiative dedicated to creating trained compliance support professionals for MSMEs.

Why Has the Government Introduced Corporate Mitras?

The Guidelines recognise an important practical reality.

India has millions of MSMEs spread across urban, semi-urban and rural areas. While large companies routinely engage Chartered Accountants, Company Secretaries, Cost Accountants and Advocates, many small enterprises lack access to affordable professional support for routine compliance matters.

Non-compliance often results not from deliberate violations but from lack of awareness, inadequate documentation and limited access to professional guidance.

The Government therefore proposes to create a cadre of trained Corporate Mitras who can assist MSMEs in routine compliance functions while enabling businesses to concentrate on growth and innovation.

Objectives of the Scheme

According to the Guidelines, the principal objectives are to:

- create a skilled pool of accredited para-professionals;

- improve regulatory compliance among MSMEs;

- simplify ease of doing business;

- generate employment opportunities for graduates;

- strengthen corporate governance practices; and

- standardise compliance support through structured training and certification.

What Services Will Corporate Mitras Provide?

The Guidelines indicate that Corporate Mitras are expected to assist MSMEs in areas such as:

- Regulatory compliance

- GST compliance

- Accounting support

- Financial guidance

- Cost accounting

- Secretarial services

- Corporate governance support

The emphasis is on supporting businesses in routine compliance activities rather than performing statutory professional functions.

Eligibility Criteria

To participate in the first batch of the scheme, candidates must satisfy the following conditions:

Particular | Requirement |

Nationality | Indian Citizen |

Age | Up to 30 years |

Qualification | Graduate or Final-Year Graduate Student |

Batch Size | 2,000 candidates (including 200 from North-East Region) |

Admissions will initially be made on a first-come-first-served basis.

Structure of the Programme

The Corporate Mitra programme extends over twelve months and consists of two distinct phases.

Academic Training

The first six months comprise structured online learning of approximately 150 hours, including webinars and interactive sessions.

On-the-Job Training

The second phase consists of six months’ practical training in recognised professional firms, providing candidates with exposure to real-life business and compliance matters.

Assessment and Certification

Certification will not depend solely on a final examination.

The evaluation consists of:

- 10% module assessments

- 50% final academic assessment

- 40% evaluation during practical training

Candidates must obtain a minimum of 50% marks and successfully complete the practical training to receive the Corporate Mitra Certificate.

Implementation Through Professional Institutes

One of the most significant aspects of the Guidelines is that the Government has chosen not to create an entirely new institution.

Instead, implementation has been entrusted to India’s three premier professional institutes:

The Institute of Chartered Accountants of India (ICAI)

The Institute of Company Secretaries of India (ICSI)

The Institute of Cost Accountants of India (ICMAI)

The programme will operate through the SWAYAM Plus Portal (https://swayam-plus.swayam2.ac.in/) , while the professional institutes will oversee training, certification and practical implementation.

Professional Firms Become Key Stakeholders

The Guidelines envisage an active role for recognised professional firms.

Candidates will undergo six months’ practical training in firms recognised by ICAI, ICSI or ICMAI.

These firms are expected to:

- provide practical exposure;

- supervise trainees;

- assess performance; and

- pay the prescribed stipend during the training period.

This approach integrates Corporate Mitras into the existing professional ecosystem rather than creating an independent parallel system.

Does the Scheme Address Earlier Concerns?

When the proposal was announced in the Union Budget, some professionals expressed apprehension that Corporate Mitras might dilute the role of qualified Chartered Accountants, Company Secretaries and Cost Accountants.

The Guidelines provide greater clarity.

Several features suggest that Corporate Mitras are intended to function as trained compliance facilitators, not as substitutes for qualified professionals.

Their training is supervised by recognised professional institutes. Practical exposure is provided through recognised professional firms. Certification is awarded only after completing both academic learning and practical training.

The Guidelines also describe Corporate Mitras as paraprofessionals, indicating a supportive rather than independent professional role.

What Does This Mean for MSMEs?

For MSMEs, the scheme offers several potential benefits.

Smaller businesses may gain easier access to trained personnel capable of assisting with:

- routine statutory filings;

- documentation;

- accounting support;

- GST compliance;

- maintenance of records; and

- basic governance practices.

This could reduce compliance gaps and encourage greater regulatory discipline, particularly in Tier-II and Tier-III cities.

Practical Issues That Remain

While the Guidelines answer many questions, several practical issues will become clearer only after implementation.

For example:

- Will the initial intake of only 2,000 candidates meet national demand?

- How will uniform quality be maintained across training firms?

- What mechanisms will ensure effective supervision during practical training?

- Will MSMEs actively engage Corporate Mitras after certification?

- Will the scope of Corporate Mitras expand in future based on industry experience?

These questions will likely shape the future evolution of the scheme.

Our Analysis

The Corporate Mitra Scheme represents a thoughtful attempt to strengthen India’s compliance infrastructure while simultaneously creating employment opportunities for graduates.

Equally significant is the Government’s decision to implement the scheme through established professional institutions rather than creating a separate regulatory framework. This approach recognises the expertise and institutional capacity of ICAI, ICSI and ICMAI while ensuring that Corporate Mitras receive structured training and practical supervision.

At the same time, the Guidelines indicate that Corporate Mitras are intended to supplement—not replace—the services rendered by qualified professionals. Statutory audits, legal representation, certification, insolvency assignments, corporate restructuring, litigation and other specialised professional functions continue to remain governed by the respective statutes regulating those professions.

The ultimate success of the scheme will depend upon the quality of training, effective supervision by professional firms and the confidence that MSMEs place in this newly created cadre of compliance facilitators.

Conclusion

With the issuance of the Corporate Mitra Guidelines, 2026, the Ministry of Corporate Affairs has moved the scheme from the realm of policy into implementation. The Guidelines provide the operational framework necessary to train, certify and deploy Corporate Mitras across the country in support of India’s MSME sector.

The coming years will determine whether the scheme succeeds in achieving its twin objectives of strengthening MSME compliance and enhancing employment opportunities for young graduates. If implemented effectively, it has the potential to become a significant component of India’s corporate compliance ecosystem while complementing the work of established professionals.