Table of Contents

ToggleHas the Bank Initiated Section 14 Proceedings? Understanding What Comes Next

Many borrowers first realise the seriousness of a SARFAESI case when they receive information that the bank has approached the District Magistrate under Section 14 of the SARFAESI Act, 2002.

A common question is:

“Does this mean the bank is about to take my property?”

The short answer is:

Possibly yes, but understanding the process and available legal remedies is important.

Section 14 proceedings generally represent a significant step towards the bank obtaining physical possession of the secured asset.

What Is Section 14 of the SARFAESI Act?

After issuing:

* Section 13(2) Demand Notice, and

* Taking measures under Section 13(4),

the bank may approach the District Magistrate or Chief Metropolitan Magistrate seeking assistance in obtaining physical possession of the secured asset.

Section 14 provides the legal mechanism through which the bank can obtain administrative and police assistance for taking possession.

Why Does the Bank File a Section 14 Application?

In many cases, the bank has already taken symbolic possession under Section 13(4).

However, symbolic possession alone may not enable the bank to:

* Enter the property.

* Remove occupants.

* Secure physical control.

* Prepare the property for auction.

Section 14 is therefore commonly used when physical possession is required.

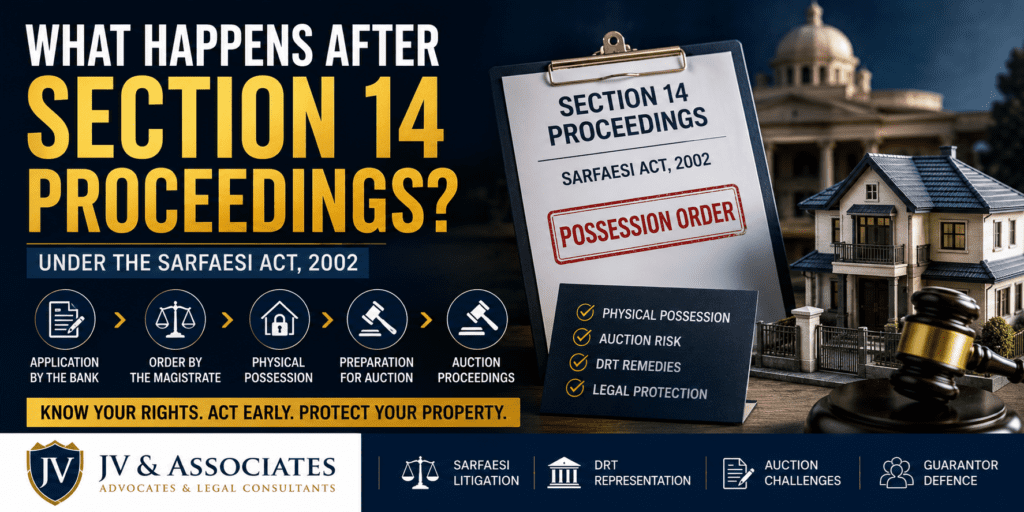

What Happens After the Section 14 Application Is Filed?

Step 1 – Scrutiny by the Magistrate

The Magistrate examines whether the statutory requirements have been complied with.

The proceedings are generally not intended to function as a full trial regarding the loan dispute.

Step 2 – Order Under Section 14

If satisfied, the Magistrate may pass an order authorising possession proceedings.

In many cases, an Advocate Commissioner or other authorised officer may be appointed to assist in taking possession.

Step 3 – Possession Notice or Communication

The borrower may receive:

* Notice from the Advocate Commissioner.

* Notice regarding proposed possession.

* Communication regarding execution of the order.

Many borrowers mistakenly assume that this is the first stage of SARFAESI proceedings. In reality, the matter has usually progressed significantly by this point.

Step 4 – Physical Possession

Officials may visit the property to:

* Take possession.

* Prepare inventories.

* Secure the premises.

* Change locks if necessary.

The exact process varies depending on the nature of the property and circumstances.

Step 5 – Preparation for Auction

Once possession is secured, the bank may proceed with:

* Valuation.

* Fixing reserve price.

* Publication of auction notice.

* Conduct of auction.

Can a Borrower Challenge Section 14 Proceedings?

Yes.

One of the most common misconceptions is that borrowers have no remedy once Section 14 proceedings begin.

In appropriate cases, borrowers may approach the Debt Recovery Tribunal (DRT) and challenge the SARFAESI measures.

The available remedy depends upon:

* Facts of the case.

* Timing of the challenge.

* Nature of the alleged illegality.

Common Grounds Raised by Borrowers

1.Defective SARFAESI Proceedings

Examples include:

* Defective notices.

* Procedural violations.

* Non-compliance with statutory requirements.

2.Incorrect Outstanding Amount

Borrowers may dispute:

* Interest calculations.

* Accounting entries.

* Amount claimed by the bank.

3.Wrongful NPA Classification

In certain situations, the borrower may challenge the basis on which the account was classified as a Non-Performing Asset (NPA).

4.Property Not Amenable to SARFAESI Action

The nature and status of the property may become relevant in some cases.

5.Serious Procedural Irregularities

Failure to follow mandatory legal procedures can become an important issue in SARFAESI litigation.

Can the DRT Stay Physical Possession?

Depending upon the facts and circumstances, borrowers may seek appropriate interim relief before the Debt Recovery Tribunal.

Every case is different and there is no automatic stay merely because proceedings have been challenged.

Prompt legal action is often important.

What If Physical Possession Has Already Been Taken?

Many borrowers assume that all remedies end once possession is taken.

That is not necessarily correct.

Depending on the facts:

* SARFAESI measures may still be challenged.

* Auction proceedings may be challenged.

* Subsequent actions of the bank may be examined by the DRT.

However, delay can significantly affect the available remedies.

What Happens After Possession Is Taken?

The typical sequence is:

- Section 13(2) Notice.

- Section 13(4) Possession Notice.

- Section 14 Proceedings.

- Physical Possession.

- Valuation of Property.

- Auction Notice.

- Auction Sale.

- Sale Certificate.

For this reason, Section 14 proceedings are often viewed as the stage immediately preceding auction.

Common Mistakes Borrowers Make

Waiting Until the Auction Notice

Many borrowers seek legal advice only after the auction has already been scheduled.

- Ignoring Communications From the Commissioner

- Notices from an Advocate Commissioner should never be ignored.

- Assuming That Physical Possession Ends All Remedies

- The legal position is often more nuanced.

- Relying Solely on Verbal Discussions

- Informal discussions with bank officials may not stop statutory proceedings.

- When Should You Seek Legal Advice?

You should consider obtaining legal advice if:

* Section 14 proceedings have been initiated.

* An Advocate Commissioner has contacted you.

* Physical possession is likely.

* The bank is preparing for auction.

* You are a borrower, guarantor, or property owner affected by the proceedings.

At this stage, time becomes an important factor.

If Section 14 proceedings have been initiated against your property, obtaining legal advice at an early stage may help you understand the available remedies and options under law.