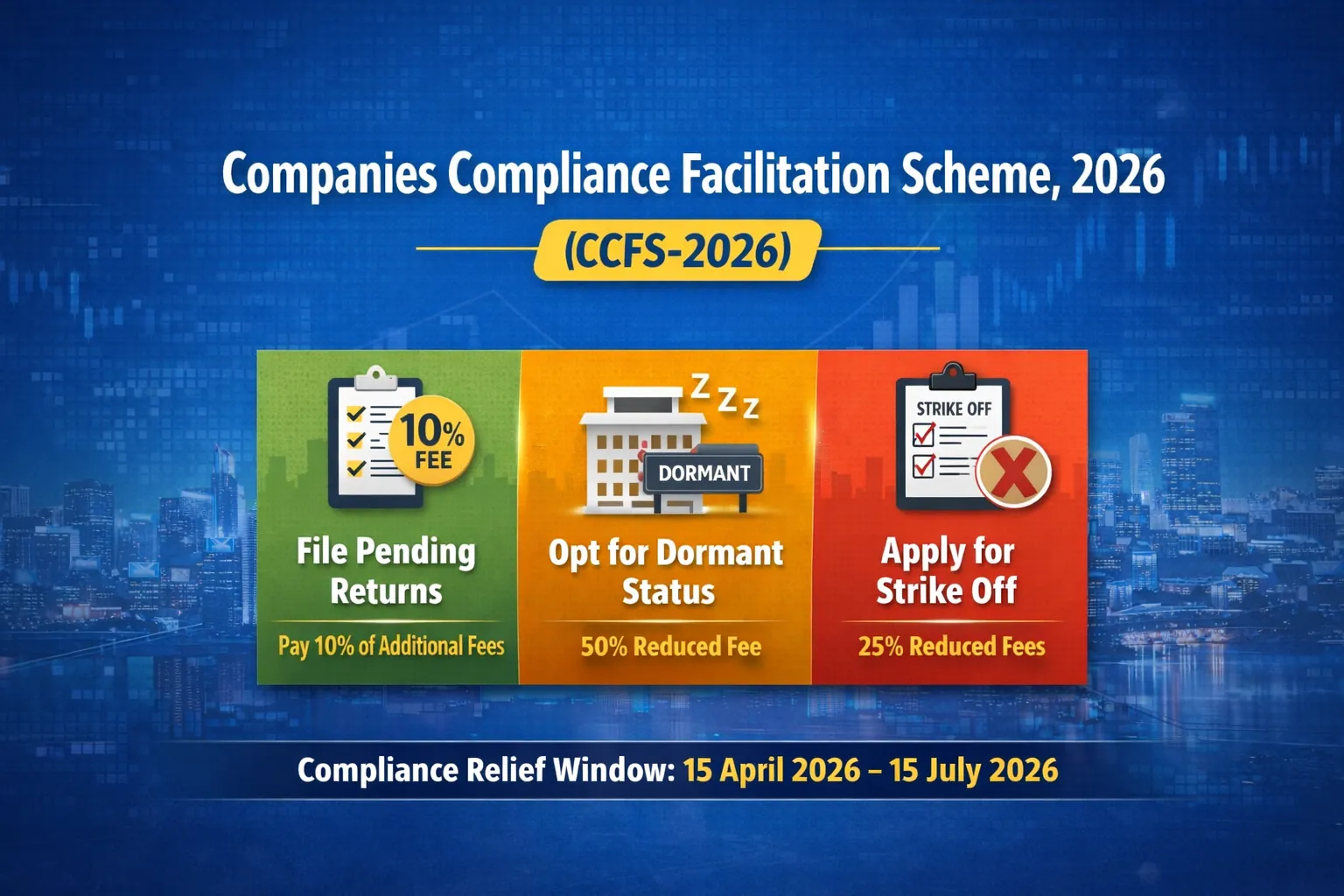

The Ministry of Corporate Affairs (MCA) has introduced the Companies Compliance Facilitation Scheme, 2026 (CCFS-2026) through General Circular No. 01/2026 dated 24 February 2026 .

This Scheme offers a time-bound compliance relief window enabling companies to:

Regularise pending annual filings at substantially reduced additional fees,

Obtain dormant status at concessional rates, or

Strike off defunct entities at a fraction of the prescribed filing fees.

For companies carrying accumulated compliance defaults, CCFS-2026 presents a structured opportunity to reset regulatory standing and mitigate financial exposure.

Table of Contents

ToggleBackground: Why Was CCFS-2026 Introduced?

Under the Companies Act, 2013, every company is required to file:

Annual Return (Section 92)

Financial Statements (Section 137)

Pursuant to Section 403 read with the Companies (Registration Offices and Fees) Rules, 2014, delayed filing attracts an additional fee of ₹100 per day without any upper cap (effective 1 July 2018) .

Over time, this resulted in significant additional fee liabilities, particularly affecting:

MSMEs

Startups

Private limited companies

One Person Companies (OPCs)

Producer companies

Inactive or defunct entities

The MCA acknowledged stakeholder representations regarding accumulated additional fee burdens and has therefore exercised its powers under Sections 460 and 403 of the Companies Act, 2013 to introduce this one-time condonation and facilitation measure.

Scheme Period

The Scheme is operational from:

15 April 2026 to 15 July 2026

This is a strict three-month window. Post-closure, normal enforcement mechanisms will resume.

Key Benefits Under CCFS-2026

1. Filing of Pending Annual Returns and Financial Statements

Companies may file pending statutory forms by paying:

Normal filing fee, and

Only 10% of the total additional fees otherwise payable

This is a substantial financial concession considering the uncapped ₹100 per day additional fee regime.

2. Dormant Company Status Under Section 455

Inactive companies may apply for dormant status by filing e-Form MSC-1.

Under CCFS-2026:

Only 50% of the normal filing fee is payable

Dormant status allows companies to remain legally registered while complying with minimal ongoing obligations.

3. Strike Off (Closure of Company)

Companies wishing to voluntarily close operations may file e-Form STK-2.

Under the Scheme:

Only 25% of the prescribed filing fee under the Companies (Removal of Name of Companies from the Register of Companies) Rules, 2016 is payable.

This offers an economical exit route for non-operational companies.

Which Forms Are Covered?

The Scheme applies to “relevant e-forms” due for filing under both the Companies Act, 2013 and the Companies Act, 1956.

Under the Companies Act, 2013

MGT-7 / MGT-7A (Annual Return)

AOC-4 (including CFS, NBFC, XBRL variants)

ADT-1

FC-3, FC-4

Under the Companies Act, 1956

Form 20B

Form 21A

Form 23AC / 23ACA

XBRL variants

Form 66

Form 23B

It is important to note that the Scheme is specifically structured around annual return and financial statement related filings and certain associated forms.

Who Is Not Eligible?

The following companies cannot avail the Scheme :

Companies against which final notice under Section 248 (strike off) has already been initiated.

Companies that have already filed for strike off.

Companies that applied for dormant status before the Scheme commenced.

Companies dissolved pursuant to amalgamation.

Vanishing companies.

Eligibility assessment must therefore be undertaken carefully before proceeding.

Immunity from Penalty: What You Must Know

The Scheme provides limited immunity in specific circumstances.

Immunity Applies Where:

Filing is made before issuance of adjudication notice; or

Filing is made within 30 days from issuance of such notice.

In such cases:

Proceedings under Sections 92 and 137 shall be concluded.

No penalty shall be levied .

Immunity Does Not Apply Where:

30 days from issuance of notice have already expired; or

An adjudication order imposing penalty has already been passed.

In such cases:

Filing fee concession applies.

Penalty liability remains unaffected.

For certain forms (ADT-1, FC-3, FC-4 and specified legacy forms), immunity is available only if no prosecution has been filed and no show cause notice has been issued before filing under the Scheme.

Post-Scheme Enforcement

After 15 July 2026, the Registrars of Companies will initiate necessary action against defaulting companies that fail to avail the Scheme

This signals stricter enforcement following the compliance window.

Frequently Asked Questions (FAQs)

1. Is CCFS-2026 applicable to LLPs?

No.

The Scheme applies only to “companies” as defined under Section 2(20) of the Companies Act, 2013 .

Limited Liability Partnerships (LLPs) are governed by the LLP Act, 2008 and are not covered under this circular.

2. Does the Scheme apply to all types of companies?

Yes, subject to eligibility conditions.

It applies to:

Private Limited Companies

Public Limited Companies

One Person Companies (OPCs)

Producer Companies

Section 8 Companies

Foreign Companies (for relevant forms such as FC-3 and FC-4)

However, companies falling within the exclusion list (e.g., final strike-off initiated, vanishing companies) are not eligible.

3. Are all company forms covered?

No.

Only the “relevant e-forms” specified in the circular are covered .

These primarily relate to:

Annual returns

Financial statements

Certain associated compliance forms

Other unrelated statutory filings (e.g., charge filings, allotment filings, DIR-related filings, etc.) are not automatically covered unless specifically falling within the notified list.

4. Does the Scheme waive penalties already imposed?

No.

If an adjudication order imposing penalty has already been passed, the penalty remains payable. The Scheme only reduces additional filing fees; it does not nullify concluded penalty orders .

5. Can a company both regularise filings and later apply for strike off?

Yes, strategically this may be advisable in certain cases.

A company may first regularise compliance to clean up its record and then apply for strike off during the Scheme period by paying 25% of the filing fee for STK-2.

Professional structuring is recommended to evaluate tax, liability, and litigation exposure before choosing this route.

6. What happens if a company does not avail the Scheme?

Post 15 July 2026:

The Registrar of Companies may initiate action.

Prosecution and adjudication proceedings may follow.

Directors may face disqualification risks in extreme cases.

The Scheme is therefore best viewed as a final opportunity before enforcement intensifies.

7. Is there any cap on the benefit available?

Yes.

The benefit is limited to:

10% of additional fees for delayed filings,

50% of normal fee for dormant application,

25% of filing fee for strike off.

Normal filing fees remain payable.

Strategic Advisory Perspective

From a regulatory standpoint, CCFS-2026 is not merely a concession — it is a compliance reset mechanism.

Companies should conduct an immediate:

Compliance gap assessment

Additional fee computation

Litigation and adjudication status review

Strategic decision analysis (revival vs dormancy vs closure)

Early action is critical because documentation preparation, financial statement finalisation, auditor coordination, and director approvals may require time.

Conclusion

The Companies Compliance Facilitation Scheme, 2026 provides a structured, financially beneficial opportunity to address long-standing compliance defaults.

For active companies, it offers a chance to restore clean compliance status.

For inactive companies, it provides economical dormancy or closure options.

For directors and stakeholders, it reduces long-term regulatory risk.

Given its limited duration (15 April 2026 to 15 July 2026), timely professional advice and structured execution are strongly recommended.